The Indian economy is estimated to grow at 5% in 2019-20 as against 6.8% in the previous fiscal

As per the latest data released by National Statistical Office (NSO) today, i.e., Tuesday, January 7, 2020, the Indian economy is estimated to grow at 5% in 2019-20 as against 6.8% in the previous fiscal.

The major factor for the downfall has been the slump witnessed in the manufacturing sector. The manufacturing sector is expected to come down to 2% in 2019-20 as compared to 6.2% in the previous fiscal. Real GDP or GDP at Constant Prices (2011-12) in the year 2019-20 is expected to attain a level of Rs. 147.79 lakh crore, as against the provisional estimate of GDP for the year 2018-19 of Rs. 140.78 lakh crore.

The first estimated growth of real Gross Value Added (GVA) in 2019-20 stood at 4.9% as against 6.6% in 2018-19. The estimates are based on benchmark indicators, such as the Index of Industrial Production (IIP), which are the approximate sector-wise calculations used to determine the health of an economy. This also includes the performance of listed private companies and crop production estimates.

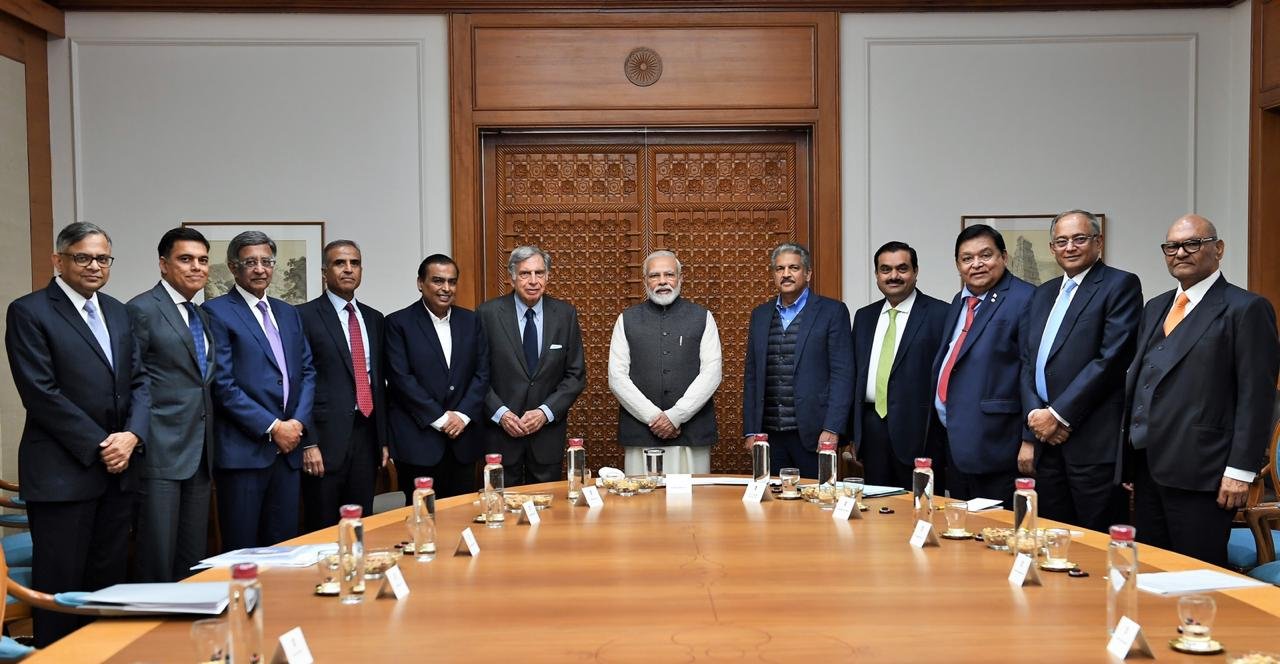

Prior to this, on January 6, 2019, in order to revive the falling economy and create jobs for youth, the Prime Minister of India – Narendra Modi held a meeting with leading industrialists in Delhi.

The industry stalwarts present in the meeting were Chairman & Managing Director (MD) of Reliance Industries Limited (RIL) – Mukesh Ambani, Former Chairman of Tata Sons – Ratan Tata, Chairman & Founder of Adani Group – Gautam Adani, Chairman of Mahindra Group – Anand Mahindra, Founder & Chairman of Bharti Enterprises – Sunil Mittal and Chairman of Vedanta Resources Limited – Anil Agarwal.

Also present in the meeting were Chairman of TVS Group – Venu Srinivasan, Group Chairman of Larsen & Toubro (L&T) Limited – A.M. Naik and Chairman of Tata Sons – N. Chandrasekaran.

The Government has so far failed to take adequate steps to revive the economy. India’s GDP growth for the July – September 2019 quarter fell to 4.5%, down from 5% as compared to April – June 2019 quarter. The Indian economy fell for the 6th straight quarter.

The 8 core industries of electricity, steel, refinery products, crude oil, coal, cement, natural gas and fertilisers contracted for the 4th consecutive month in November 2019, by 1.5%. What’s more disturbing is that these 8 core industries have been recording negative growth since August 2019.

The credit crunch among Non-Banking Financial Companies (NBFCs), inability of Government agencies in tackling the economic crisis, prolonged financial stress among rural households, have also led to the downfall of Indian economy.

This is despite Modi Government undertaking a number of measures such as reduction in corporate tax to 22% from 30%, lowering of tax for new manufacturing companies to 15% to attract new Foreign Direct Investments (FDI), bank recapitalization, the mergers of 10 public sector banks into 4, support for the auto sector, plans for infrastructure spending, as well as tax benefits for start-ups.

As per the analysts, a GDP of nearly 12% is required to make India a U.S. $ 5 trillion economy by 2024-25. All the eyes are now on the Finance Minister of India – Nirmala Sitharaman, who is likely to present her 2nd Union Budget on February 1, 2020.