The Union Minister for Finance and Corporate Affairs, Shri Arun Jaitley chairing the 22nd GST Council meeting, in New Delhi on October 06, 2017.

The Minister of State for Finance, Shri Shiv Pratap Shukla, the Revenue Secretary, Dr. Hasmukh Adhia, the Chief Economic Adviser, Dr. Arvind Subramanian and other dignitaries are also seen. Credit: Press Information Bureau, Government of India

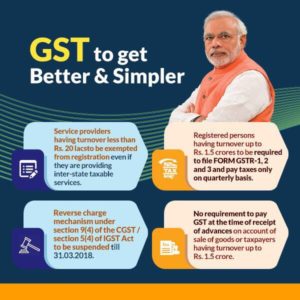

Yesterday the government announced big changes to the GST regime in India. It has been decided that within the next 4 days the held-up refund of IGST paid on goods exported outside India in July would begin to be paid. Further to prevent cash blockage of exporters due to upfront payment of GST on inputs etc. the Council approved two proposals, one for immediate relief and the other for providing long term support to exporters. Immediate relief is being given by extending the Advance Authorization (AA) / Export Promotion Capital Goods (EPCG) / 100% EOU schemes to sourcing inputs etc. from abroad as well as domestic suppliers. Holders of AA / EPCG and EOUs would not have to pay IGST, Cess etc. on imports.

Also to restore the lost incentive on sale of duty credit scrips, the GST on sale-purchase of these scrips is being reduced from 5% to 0%.

In a big relief for jewellery sector has been announced and the need for PAN card for purchases above 50,000 Rs has been removed.

In a major overhaul quite a few flaws of the present GST implementations have been taken head on.

When it comes to GST, it seems that the BJP led government in center has learned a lot from Microsoft. Like the Software mammoth, government released a buggy implementation and now we are thanking them for fixing the bug. Not that we are any less thankful for ‘fixing these problems.

The Teething troubles of GST had ended up with Exporters waiting for 65,000 crore of their working capital to be returned by government in due course. Further frequent changes of tax rates coupled with arbitrary penalization by authorities for not wrong GST assessment has created a prosecution among small business along with a very real chance of going wrong.

Further the period of only 60 days to rectify a input tax mismatch is highly impractical. For example – if I have a vendor who provides an advance invoice for services delivered to me doesn’t pay his GST, my input credits for his services are denied. Given the fact in 60 day period it’s not feasible for me to insure that my vendor has paid his tax and that my input credit is not denied. Further after this 60 day period if the vendor pays his due, my input credits are still nowhere to be seen. So in effect I will be penalized by 100% of input tax for delays by my vendor.

Then there was the problem of input tax credit on input services related to immovable property. For businesses based in Delhi-NCR, there is a lot expenses that are divided between Delhi, Haryana, UP and Rajasthan. Now the present laws suggest that if your business is not based in the same state as that of your supplier then you cannot claim SGST part of the expenses. Now to claim this one has to open. For the business to claim the credit, it would have to get a Goods and Services Tax registration in all four of Delhi, Rajasthan, UP and Haryana. For each registration every business will have to file three returns a month and another three returns annually. This implies a total of 156 returns. For a company working on national level this would be 1404 returns annually. No doubt that the demand for accountants is all set to increase.

While the changes brought forward by the GST Council meet of 6 October 2017 have fixed a few of the problems – a lot more is desirable and it might well be GST itself, much like our analogy of windows software, may always remain a work in progress